Golden Rules of Accounting Made Simple

Master the 3 golden rules—Personal, Real & Nominal—and learn how to pass journal entries with ease. Perfect for CA Foundation beginners!

CA FOUNDATION

9/12/20252 min read

The Golden Rules of Accounting: A Beginner's Guide to Journal Entries

Accounting is often called the “language of business,” and like any language, it has its own grammar and rules. For beginners—especially CA Foundation aspirants—the Golden Rules of Accounting form the base of all financial recording. Understanding these rules makes it easier to create journal entries, which are the first step in the accounting process. Let’s decode these rules in a simple way.

Why Golden Rules of Accounting Matter

Every business records thousands of transactions daily—purchases, sales, expenses, investments, and more. Without proper rules, recording these entries would be chaotic. The Golden Rules bring clarity, consistency, and universal application, ensuring that financial records are reliable and understandable.

The Three Types of Accounts in Accounting

To apply the Golden Rules, you must first know the three types of accounts:

Personal Account: Relates to persons or entities (e.g., debtors, creditors, banks).

Real Account: Relates to tangible and intangible assets (e.g., cash, furniture, patents).

Nominal Account: Relates to expenses, incomes, losses, and gains (e.g., rent, salary, commission).

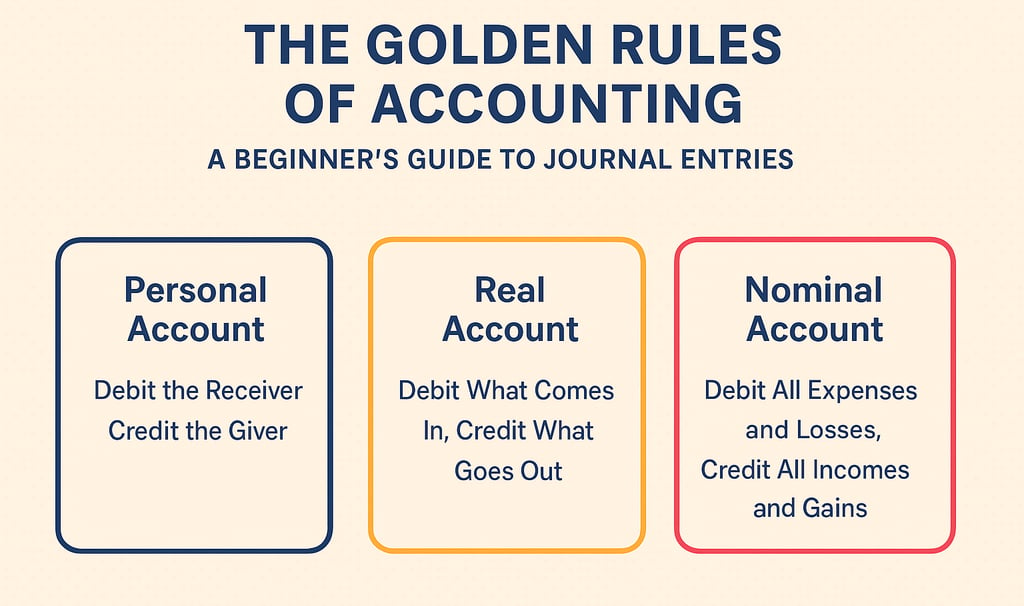

The Golden Rules of Accounting

Personal Account – Debit the Receiver, Credit the Giver.

Example: If you pay ₹5,000 to a supplier, the supplier’s account (giver) is credited, and your cash account is debited.Real Account – Debit What Comes In, Credit What Goes Out.

Example: Buying furniture for ₹10,000 means furniture (comes in) is debited, while cash (goes out) is credited.Nominal Account – Debit All Expenses and Losses, Credit All Incomes and Gains.

Example: Paying salary of ₹15,000 is debited to Salary Account (expense), and cash is credited.

How to Apply the Rules in Journal Entries

Journal entries record every transaction in a debit-credit format. A standard entry includes:

Date of transaction

Particulars (accounts involved)

Debit and credit amounts

Narration explaining the transaction

By applying the Golden Rules, you can decide instantly which account to debit and which to credit.

Common Mistakes Beginners Make

Mixing up nominal and real accounts.

Forgetting that cash is also a real account.

Overcomplicating entries instead of sticking to basics.

Ignoring narrations, which are vital for clarity.

Tips to Master Journal Entries

Practice daily with real-life examples like paying rent, buying stationery, or depositing cash in bank.

Revise the rules frequently until they become second nature.

Solve past CA Foundation papers for applied practice.

Work with ledgers after journal entries to see the bigger picture of accounting.

Final Thoughts

The Golden Rules of Accounting are the foundation of all bookkeeping. Once you master them, creating journal entries becomes a simple, logical process. For CA aspirants, this clarity builds confidence and helps in solving even complex accounting problems later.

At ResultPrep, we train students with step-by-step accounting exercises, solved journal entry examples, and practice worksheets, so that the basics are strong from day one.

Prepare for the best results!

Achieve your goals with expert coaching and support from ResultPrep.

Contact us:

© 2025. All rights reserved.

Address:

GSS Complex, 2nd Floor,

16th Cross Rd, HMT Layout, Vidyaranyapura, Bengaluru, Karnataka- 560097