Non-Profit Organisation Accounting Made Easy: Rules, Statements & Exam Tips!

Confused about NPO Accounting? 🤔 Learn everything — from Receipts & Payments to Income & Expenditure and Balance Sheet preparation — with simple explanations, real examples, and exam-focused insights. Perfect for CA Foundation and Class 12 students, this guide explains donations, subscriptions, depreciation, and fund-based accounting clearly. Master NPO concepts and score full marks in your next accounting exam! 💯✨

CA FOUNDATION

10/11/20254 min read

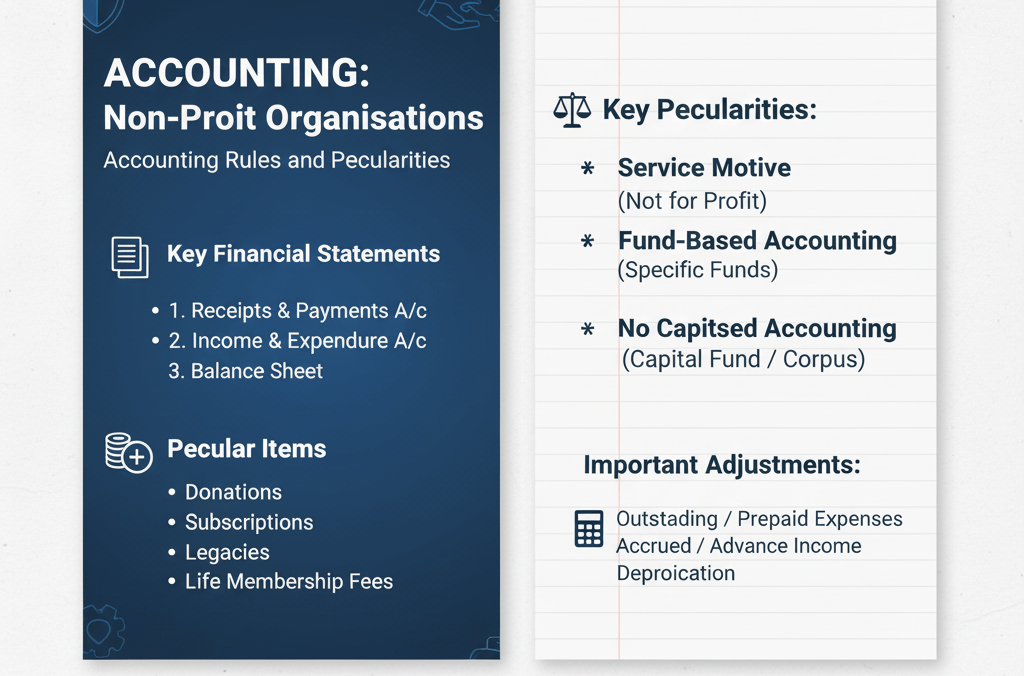

Accounting: Non-Profit Organisations — Accounting Rules and Peculiarities

Non-Profit Organisations (NPOs) play an important role in society by serving public causes rather than earning profits. These include schools, hospitals, charitable trusts, sports clubs, religious institutions, and welfare societies. While their purpose is not profit generation, they still need to maintain systematic records of income, expenses, assets, and liabilities. Accounting for Non-Profit Organisations follows specific rules and conventions to ensure transparency, accountability, and compliance. In this blog, we will explore the key accounting rules, financial statements, and peculiarities that make NPO accounting different from business accounting — a topic crucial for CA Foundation and Class 12 students alike.

Understanding Non-Profit Organisations

A Non-Profit Organisation operates with the primary objective of promoting social, cultural, educational, or charitable activities. It receives funds through donations, grants, subscriptions, or legacies, which are used for achieving its objectives rather than distributing profits. Any surplus generated is reinvested to further its goals.

Need for Accounting in NPOs

Even though NPOs are not profit-driven, they must maintain proper books of accounts for several reasons — ensuring accountability to donors and members, maintaining transparency in fund usage, assessing financial health and sustainability, and fulfilling statutory and audit requirements.

Key Accounting Characteristics of NPOs

Unlike businesses that prepare a Trading and Profit & Loss Account, Non-Profit Organisations prepare three main financial statements: (1) Receipts and Payments Account, (2) Income and Expenditure Account, and (3) Balance Sheet. These records help present an accurate picture of financial activities during a particular period.

1. Receipts and Payments Account

It is a real account that records all cash and bank transactions, whether of capital or revenue nature, during a financial year. The receipts side includes all cash inflows such as donations, subscriptions, entrance fees, and grants. The payments side includes all outflows such as rent, salaries, honorarium, maintenance, and purchases. It is similar to a cash book and shows the closing cash or bank balance at year-end. Importantly, it does not distinguish between revenue and capital items, nor does it consider accruals or outstanding amounts.

2. Income and Expenditure Account

This is similar to a Profit & Loss Account in business organisations but serves a different purpose. It records all revenue incomes and expenses of the current year on an accrual basis. Non-cash items like depreciation and outstanding expenses are also considered. The difference between income and expenditure is termed as surplus (if income > expenditure) or deficit (if expenditure > income). For example, if a charitable hospital earns ₹10,00,000 in donations and spends ₹8,50,000 on operations, it will show a surplus of ₹1,50,000 for that year.

3. Balance Sheet

The Balance Sheet of an NPO shows its financial position on a given date. It lists all assets such as buildings, furniture, equipment, investments, and cash balances on one side, and all liabilities such as capital funds, subscriptions received in advance, and outstanding expenses on the other. The capital fund (also called the general fund) represents the accumulated surplus of the organisation over the years.

Peculiar Items in NPO Accounting

There are several accounting items unique to NPOs that require special treatment:

Donations: Donations can be of two types — general and specific. General donations are treated as income in the Income and Expenditure Account, while specific donations (like for building funds or scholarships) are treated as capital receipts and shown under liabilities in the Balance Sheet.

Subscriptions: Members’ subscriptions form an important income source. Adjustments must be made for subscriptions received in advance and outstanding subscriptions to determine the actual amount earned for the year.

Entrance Fees: Depending on the organisation’s policy, entrance fees can be treated either as revenue income or as a capital receipt.

Legacies: Amounts received under a will are capital receipts and shown in the Balance Sheet.

Life Membership Fees: Treated as a capital receipt since it is a one-time payment made by a member for lifelong benefits.

Honorarium: Payments made to individuals for their services (like guest speakers or performers) are treated as expenses.

Treatment of Depreciation and Investments

Depreciation is charged on fixed assets to account for their wear and tear, just like in business accounting. NPOs often invest their surplus funds in government securities, bonds, or bank deposits. The interest earned on such investments is treated as income and recorded in the Income and Expenditure Account.

Common Adjustments in NPO Accounts

Students must pay special attention to adjustments involving outstanding expenses, prepaid expenses, accrued incomes, and incomes received in advance. For example, if rent of ₹5,000 is outstanding, it must be added to the expenditure for the year; similarly, if interest income of ₹2,000 is accrued, it must be added to income.

Importance of Fund-Based Accounting

In larger NPOs, fund-based accounting is used to track the use of specific funds separately, ensuring that donations and grants are used only for their intended purposes. For instance, a “Building Fund” or “Sports Fund” will have separate ledgers to show receipts, payments, and balances.

Conclusion

Accounting for Non-Profit Organisations may seem different from business accounting, but the underlying principles of accuracy, transparency, and accountability remain the same. By maintaining Receipts and Payments Accounts, Income and Expenditure Accounts, and Balance Sheets properly, NPOs can ensure smooth financial management and earn the trust of donors and beneficiaries.

For CA Foundation aspirants, mastering NPO accounting is crucial — it strengthens your conceptual understanding of financial statements and helps you tackle practical questions confidently in exams.

At ResultPrep Coaching, we focus on simplifying such accounting concepts with real-life examples, guided practice, and regular mock tests to help you build accuracy and confidence.

📞 Call: 8970007497

🌐 Visit: www.resultprep.com

Prepare for the best results!

Achieve your goals with expert coaching and support from ResultPrep.

Contact us:

© 2025. All rights reserved.

Address:

GSS Complex, 2nd Floor,

16th Cross Rd, HMT Layout, Vidyaranyapura, Bengaluru, Karnataka- 560097